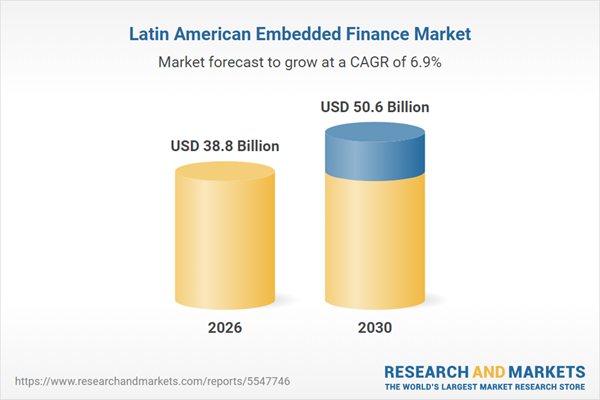

The Latin America embedded finance market is on a strong growth path, projected to expand from US$35.4 billion in 2024 to approximately US$50.6 billion by 2030. This represents a steady compound annual growth rate of 6.9% from 2026 onward. The market’s dynamism is fueled by platform-led business models and a drive to serve vast underbanked populations.

This robust growth follows a period of rapid expansion between 2021 and 2025. Key drivers include significant financial access gaps and widespread mobile-first consumer behavior. Consequently, non-financial platforms are integrating payments, credit, and insurance directly into their user experiences.

Platform-Led Models Are Driving Market Dominance

The Latin America embedded finance landscape is defined by major digital platforms that build financial services directly into their core offerings. E-commerce, delivery, and mobility giants are creating closed-loop ecosystems that compete directly with traditional banks and fintechs.

For example, Mercado Libre operates its own payment system (Mercado Pago) and credit arm (Mercado Credito). This integrated approach spans payments, credit, and insurance across key markets like Brazil, Argentina, and Mexico. Similarly, super apps like Rappi and PicPay are expanding from payments into credit cards and investments.

Embedded Credit and Super Apps Fueling Growth

Two major trends are accelerating the adoption of Latin America embedded finance: the rise of embedded credit and the expansion of super apps.

The Expansion of Embedded Credit

Digital platforms are integrating credit options directly into customer purchase journeys. Mercado Credito, for instance, extended over US$3.3 billion in loans in 2023. This model thrives because it meets the needs of a large underbanked population estimated at over 200 million people.

The Super App Ecosystem

Super apps are bundling financial services to increase user loyalty. Rappi, Nubank, and PicPay have all evolved from single-purpose apps into broad financial ecosystems. They now offer services from insurance to cryptocurrency investing, creating a one-stop-shop for users.

Regulatory Momentum and Competitive Landscape

The regulatory environment is a key factor shaping the Latin America embedded finance market. However, progress is uneven across the region.

Brazil and Mexico lead with clear regulatory frameworks. Brazil’s Open Finance initiative and Mexico’s Fintech Law provide a solid foundation for innovation. Conversely, countries like Argentina and Peru operate under more fragmented rules, which complicates market entry.

This regulatory divergence influences competition. Brazil and Mexico are the most mature and competitive markets. Meanwhile, countries like Colombia and Chile are gaining traction through localized innovation. For detailed market analysis, the full report is available from Research and Markets.

Consolidation and Infrastructure

The future of the Latin America embedded finance market points toward increased consolidation. Infrastructure providers that handle complex compliance and banking processes are becoming essential. Companies like Dock and Pomelo provide the back-end APIs that allow smaller merchants to offer financial products easily.

Furthermore, competition is expected to intensify in underpenetrated segments like agriculture and transportation. New, API-first entrants are targeting these niches with specialized solutions.

In conclusion, the Latin America embedded finance market is transitioning from rapid growth to mature, infrastructure-led competition. The continued convergence of financial and lifestyle services within super apps will redefine the regional economic landscape for the next decade.